On February 1, 2023, the Silicon Industry Branch of the China Non ferrous Metals Industry Association released the latest weekly review of silicon material prices.

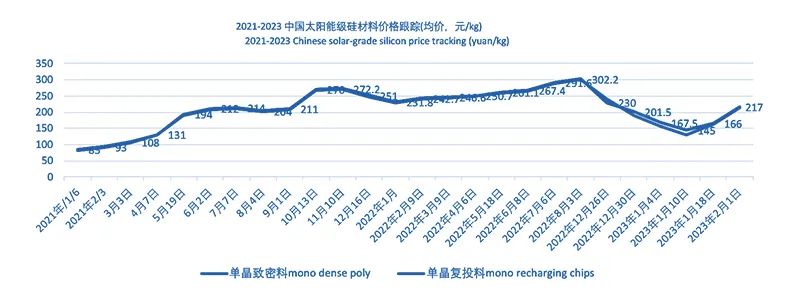

According to the public information, the domestic single crystal re feeding price range this week is between 200000 and 23200 yuan/ton, with an average transaction price of 217500 yuan/ton, representing a year-on-year price increase of 31.02% compared to the pre festival price; The price range of single crystal dense materials is 198-23000 yuan/ton, with an average transaction price of 215200 yuan/ton, a year-on-year price increase of 31.22%.

As for the main reasons for the increase in polysilicon prices this week, the Silicon Industry Branch stated that the main performance is as follows: First, the price fluctuation range this week is the result of cross week calculation, and the increase seems to be large, but it is actually the cumulative increase in prices over two weeks; Secondly, before the festival, the price of silicon wafers has taken the lead in stabilizing and rising compared to the price of silicon materials. At the same time, the operating rate of silicon wafer enterprises has also significantly increased, and the demand for silicon materials has increased significantly; Thirdly, the price of silicon materials has also begun to stabilize and recover before the festival. In addition, during the Spring Festival holiday, the raw materials of silicon wafer enterprises have been completely digested, and the demand for silicon materials procurement has increased significantly in the first week after the festival, supporting the continued upward trend of silicon prices.

In the first week after the Spring Festival, domestic polysilicon prices continued their steady upward trend before the festival. This week, the prices of various categories of silicon materials increased by about 31% compared to two weeks ago. The mainstream transaction price of single crystal dense materials was between 208-22000 yuan/ton, with the highest price reaching over 230000 yuan/ton. The number of enterprises with new orders concluded this week is about 5, and the market activity is relatively stable. The remaining enterprises that have not yet concluded transactions are also in the post holiday negotiation stage, and some orders will be confirmed within this week.

As of this week, 15 polysilicon enterprises were in production, and all maintained normal production and operation. According to the statistics of the Silicon Industry Branch, the domestic polysilicon production in January was about 101400 tons, a year-on-year increase of 4.9%. The increase was mainly reflected in the release of new capacity such as Baotou Xinyuan and Runyang New Energy, as well as the increase in the maintenance and resumption of production of Lihao Semiconductor. The subtotal was about 5000 tons, accounting for 83% of the increase in January.

Enterprises that will still have incremental releases in the first quarter include GCL Technology (Leshan+Baotou), Oriental Hope, Lihao Semiconductor, Runyang New Energy, etc. However, the monthly output growth is relatively small. It is expected that the average monthly output of polysilicon in China in the first quarter will be around 105000 tons, which can meet the average monthly output of 40GW of silicon wafers. According to the upstream and downstream production scheduling plans, it is expected that the supply and demand of silicon materials will be relatively balanced in the first quarter. With the downstream operating rate raised to normal operation and normal procurement, the price of silicon materials can basically maintain a stable operation.

However, the current market supply and demand relationship is relatively fragile. On the one hand, downstream silicon wafer companies have not yet raised their operating rates, and on the other hand, the normalization of silicon material inventory continues. There are many and scattered factors that affect market prices. It is expected that in the short term, the increase in silicon wafer operating rates and procurement demand will serve as the main driving force to support a steady rise in silicon material prices. The high point of industry chain prices can be calculated based on the general acceptance of terminal demand for component end prices.